Money Problems in Marriage: Why You're Not Really Fighting About Money

By Giulia P. Davis, LMFT | Mycelia Therapy | San Francisco, California

It's 11pm. One of you just saw the credit card statement, or the trading account, or the auto-deposit that was supposed to go to savings. The argument that follows isn't really new. It's the same one you've had four times this year, dressed in a different number.

If you're searching money problems in marriage tonight, you're probably not looking for a budget. You're looking for an explanation. You and your partner can navigate hard conversations about almost anything else: work pressure, in-laws, parenting, even sex. But money walks in, and the whole nervous system of the relationship shifts.

There's a reason for that. And it isn't a budgeting problem.

What this piece names:

Why money fights in marriage are almost never about money, and what they're actually about

The four money scripts that shape how each partner handles finances (Klontz, Journal of Financial Therapy)

Why wealth doesn't resolve money anxiety for high-earning couples, and often intensifies it

When a therapist alone isn't enough, and when to bring a financial planner into the work

Why are money problems in marriage rarely about money?

When couples come into my practice describing money problems in marriage, the presenting issue is almost never the issue. Money is one of the few topics that simultaneously touches safety, identity, power, freedom, time, status, and inherited family material. You're not fighting about a credit card charge. You're fighting about what that charge symbolizes for each of you.

Depth psychology has long understood that the things we fight about are rarely just what they seem. In a Jungian sense, money carries symbolic weight. It touches questions of safety, identity, power, and belonging that go far beyond the numbers themselves. Recurring money conflict is, in that frame, two psychological systems trying to stabilize themselves through the same object.

CASE STUDY

In one San Francisco case, a couple in their early 40s arrived with high income, two kids, and two very different money stories. She was a senior product leader who held the household together with careful tracking. Money was safety. He was a founder fresh off a partial exit, between ventures. Money was evidence of his competence.

Their arguments were not about the line items. They were about whose version of security felt valid in the room.

She would say, "I feel like I'm the only adult managing our financial life." He would say, "No matter how much I make, it's never enough for her to feel safe." The shift came mid-session when she said, "If something happens, I'm the one who will have to hold everything together." He paused, then answered, "You actually don't trust that I'd show up."

That's where the work changed. The conversation wasn't about dollars. It was about trust, history, and whether they could rely on each other when things broke.

The numbers eventually got addressed. But not until that.

The 4 money scripts shaping how you and your partner handle finances

The framework of money scripts comes from financial psychologist Brad Klontz, whose research published in the Journal of Financial Therapy identifies four dominant beliefs formed in childhood and carried, mostly unexamined, into adult relationships. Most of us have a primary and a secondary. Most couples are working with two combinations colliding in real time.

1. Money avoidance. Money is bad, corrupting, or wanting it is morally suspect. Surfaces as undercharging, avoiding accounts, guilt about success. In couples, one partner refuses to engage with planning at all.

2. Money worship. More money will solve any problem: happiness, security, self-worth, status. The script doesn't switch off when someone earns "enough." The target moves.

3. Money status. Net worth equals self-worth; money is a scoreboard. Comparison to siblings, peers, parents, prior versions of self. Purchases signal arrival rather than align with values.

4. Money vigilance. Money must be carefully tracked, protected, and not spoken about openly. Often rooted in early instability. These are the partners managing the spreadsheets, and feeling alone in it.

In the couple above, vigilance and status are colliding. She's tracking. He's signaling. Both are coherent internally. Neither makes sense to the other. The work isn't to argue who's right. It's to make the underlying scripts visible enough that they stop running the conversation from underneath.

Financial issues in marriage: what therapy research actually shows

Financial issues in marriage are one of the most consistently cited sources of relational distress in couples research. The Gottman Institute, drawing on John Gottman's research with married couples identifies money as one of the major "perpetual problems." These are conflicts that don't fully resolve. They have to be managed over the life of a relationship.

About two-thirds of long-term couple conflicts fall into this perpetual category. Money is one of the most reliably charged.

Clinically, I see Gottman's "four horsemen" of relationship breakdown show up around money faster and more intensely than around almost any other topic. Criticism, contempt, defensiveness, stonewalling. The conflict itself isn't what's destructive. How couples engage with it is.

Knowledge alone doesn't predict good financial decisions or relational stability around money. Awareness of the underlying emotional and relational pattern does. If you and your partner have access to good financial advice and you're still fighting, this is why. The problem isn't a knowledge gap.

For a deeper read on how recurring conflict masks attachment cycles, my post on whether couples therapy can resolve recurring disagreements breaks down the pattern.

The high-earner paradox: why doesn't wealth resolve money anxiety?

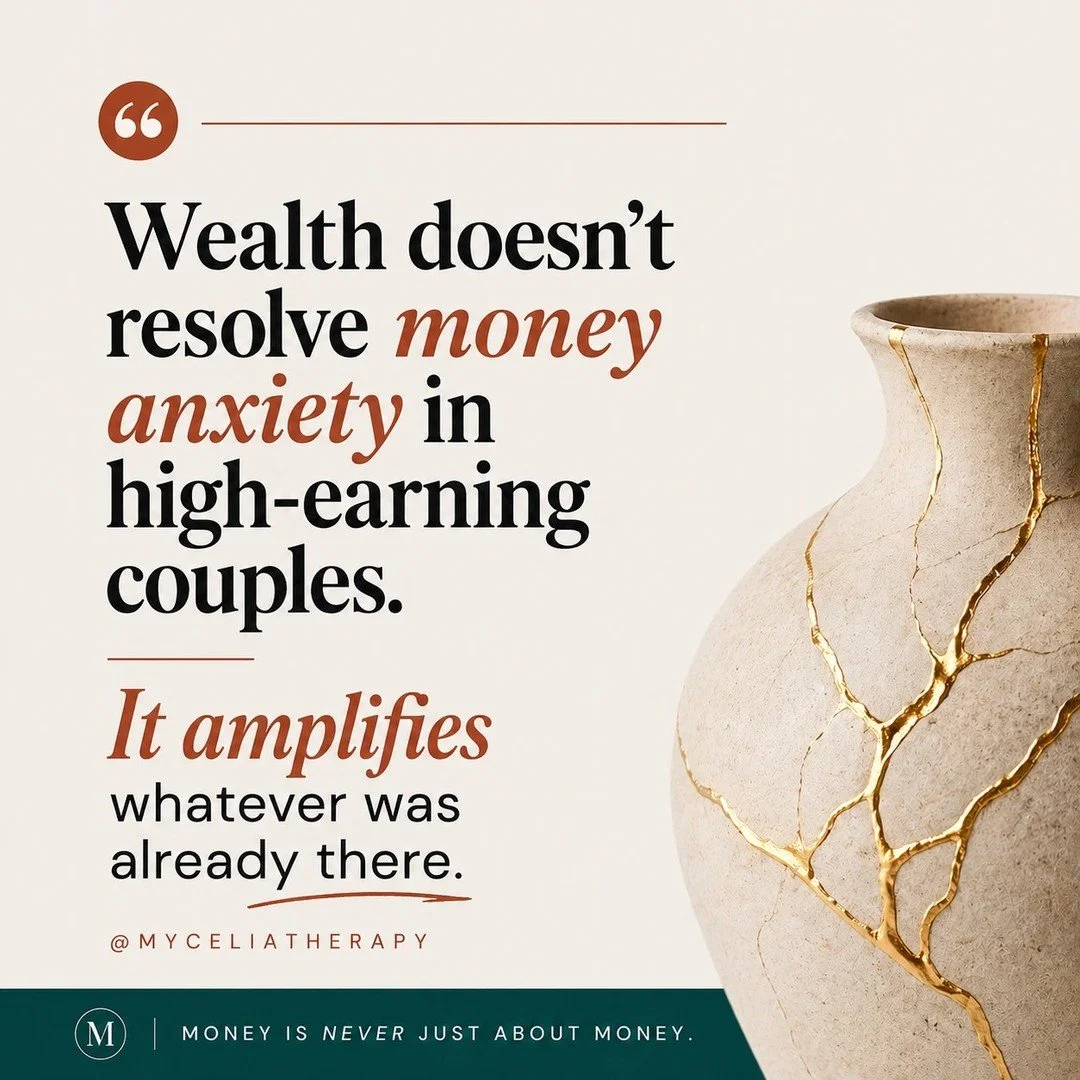

For many high-earning couples, more money has not made the anxiety go away. In some cases, it has intensified.

“Money remains a top source of conflict for nearly a third of partnered adults, and the pattern holds even at high income levels.

”

https://www.apa.org/topics/money/conflict

The higher the net worth, the less anchored many people feel.

Not because they're irrational, but because wealth expands the number of decisions, variables, and potential losses. Instead of safety, they experience heightened responsibility and a fear of irreversible mistakes.

Money in this population is doing heavier psychological work. It carries safety (often rooted in early instability that wasn't resolved by later success). It carries self-worth, particularly in identities organized around achievement ("I'm only as good as my last win"). It carries freedom, optionality, and scorekeeping against siblings, peers, or earlier versions of self. These needs are infinite. The target keeps moving.

“These needs are infinite. The target keeps moving.”

There's also the liquidity vs. net worth confusion that shows up in nearly every founder couple I see. High net worth on paper, concentrated equity or illiquid assets in reality. One partner experiences abundance. The other experiences constraint. Both are right. They're living in different financial realities under the same roof.

The most clinically relevant piece is the most invisible: the "I should be over this" shame. Many high earners feel a private anxiety they can't bring to friends (too privileged) or colleagues (too vulnerable). They often don't bring it to each other. Public competence — private destabilization. A corrosive combination in a relationship.

It's not that wealth creates dysfunction. Wealth amplifies whatever was already there.

Couples with aligned money narratives, a shared definition of "enough," and trust experience money as stabilizing, even at very high levels. Couples without those experience money as pressure, also at very high levels.

If this dynamic is familiar, my work with executives, founders, and entrepreneurs is built around it.

Financial infidelity and the rupture of trust

Financial infidelity is the deliberate concealment of financial information from a partner: hidden accounts, undisclosed debt, secret spending, or lying about income or losses.

Peer-reviewed research in the Journal of Financial Therapy documents how widespread the behavior is in committed couples, and how it correlates with lower marital satisfaction and higher conflict.

Clinically, it functions like other forms of betrayal. It activates the attachment system, creates a before-and-after rupture, and introduces hypervigilance, even though the offense is financial. It often goes unreported because both partners feel ashamed, and because there's no clear cultural script for what it means.

The rupture destabilizes the basic premise of the relationship: if you lied about this, what else? It is not about the dollar amount. It's about the fact that one partner was operating in a reality the other didn't have access to.

Most often, financial infidelity isn't cold or calculated. It starts as avoidance. A small thing not mentioned. A credit card opened "just to handle it." A loss not disclosed because the discloser couldn't bear the conversation. By the time it surfaces, both partners are dealing with the original financial issue and the rupture of trust.

Repair is possible. But it's a different kind of work than budget reconciliation. It involves the same architecture as repair after any betrayal: disclosure, accountability, capacity to tolerate the partner's pain without defensiveness, and time. It's not faster because the offense was financial.

If you're in active discovery of financial infidelity, I generally do not recommend a couples intensive as the first step. The nervous system needs to come out of acute shock first.

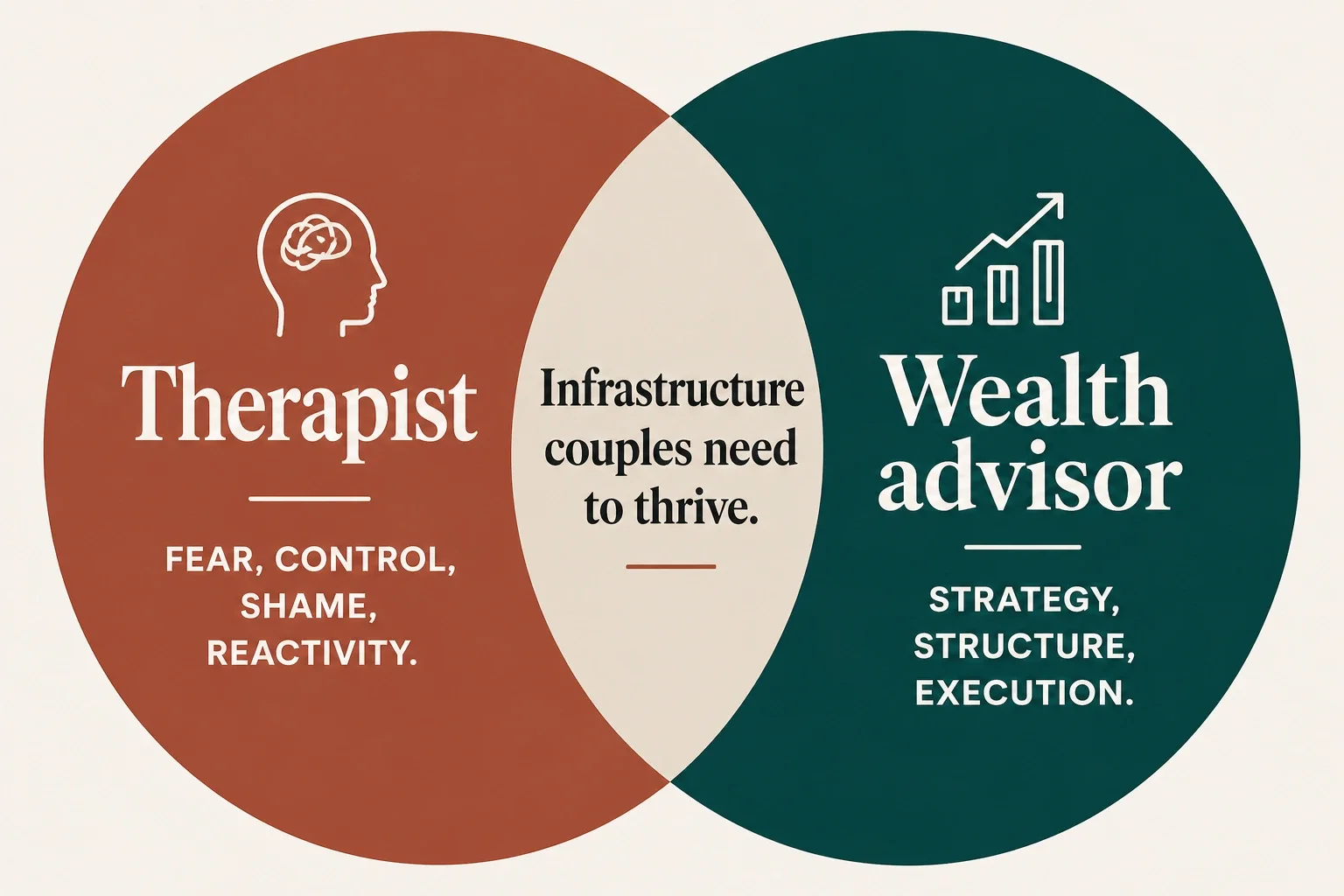

When should you bring in a financial planner, and when a therapist?

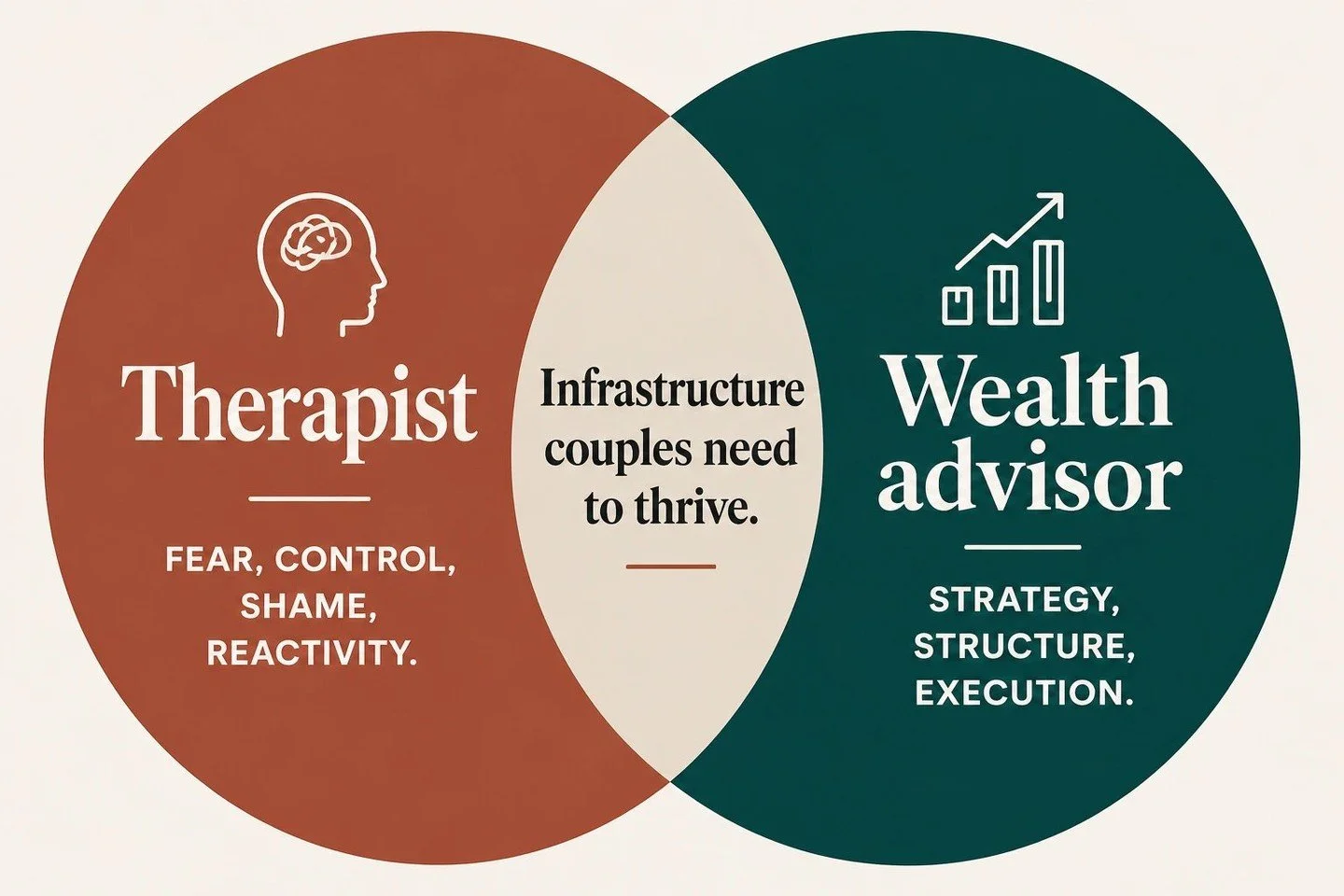

When high-earning couples come to therapy with money distress, a therapist alone or a financial advisor alone usually can't resolve it. With written client consent, I actively collaborate with clients' wealth advisors and financial planners. The therapist handles the emotional, relational, and identity-level material. The planner handles strategy, structure, and execution. Together they create the infrastructure couples need to actually thrive.

This is unusual. Most therapists work in a silo. Most financial advisors don't have training in the emotional dimensions of money. I've seen what becomes possible when those two streams of expertise are coordinated rather than separate.

How the collaboration works

The collaboration begins when the couple's money conflict is not only emotional and not only technical. Sometimes they already have an advisor they trust. Sometimes I refer them into a small network of planners I've vetted. The advisor doesn't need to be "mine." What matters: the couple trusts them, they're competent, and they understand the complexity of working with high-earning couples. Money in this population is tied to identity, safety, power, and family legacy.

What therapy handles vs. what the financial planner handles

When this model isn't the right fit

Some couples don't need it. If the conflict is purely emotional and the financial picture is already clear and aligned, additional financial input can be redundant. Couples in early discovery of financial infidelity typically benefit from sequencing therapy ahead of any planning work.

This work also gets more layered with multicultural couples. As an Italian-born clinician working with international couples in the Bay Area, I see this often. One partner may experience building wealth as responsibility. Another may experience it as disloyalty, excess, or pressure to assimilate. These aren't communication issues. They're inherited maps of survival, belonging, and identity.

The same applies, with additional structural complexity, in poly relationships, throuples, and polycules. My post on why polyamorous communication often fails and how to fix it goes deeper.

Most couples already have access to advice. What they don't have is a way to integrate it with how they actually think, feel, and relate under pressure.

Even the best wealth strategies fail if the people making the decisions can't stay steady with them.

“Even the best wealth strategies fail if the people making the decisions can’t stay steady with them.”

How can couples intensives shift entrenched money conflict?

A couples intensive — one to three concentrated days of therapy — works for couples who are entrenched in money conflict, time-constrained, or ready to focus and move on a specific issue. The format isn't inherently superior to weekly therapy; it's different. Intensives let one issue stay open long enough to actually shift, instead of getting interrupted by a 50-minute session ending and six days of stewing in between.

What an intensive allows: staying with one issue long enough for it to actually shift. Completing a rupture-and-repair arc in real time rather than letting it harden. Mapping money history and testing new agreements in one continuous thread. Bringing in the wealth advisor mid-intensive when relevant, so emotional clarity and structural decisions move together.

Couples don't walk away with perfection. They walk away with a shared understanding of what's driving the conflict. At least one significantly shifted dynamic. Clearer agreements. Meaningfully less reactivity around the topic.

For more, see my piece on the benefits of intensive couples therapy. You can also learn about the structure of my couples intensives.

How I work with couples on money in my practice

Couples counseling for money issues, in my practice, doesn't start with a budget. It starts with a question most couples have never been asked:

What is money for, for you?

Security. Freedom. Status. Time. Repair of something inherited.

Each partner has an answer. Most have never compared them.

Where the work starts

When money shows up in weekly couples work, it usually arrives as something else: resentment ("I'm carrying this alone"), control vs. avoidance, anxiety about the future, mismatched definitions of "enough." We trace it backward.

Early in the work I tend to do three things. Money history: what each of you learned about money growing up, explicitly and implicitly. Meaning mapping: what is money for for you (security, freedom, worth, care, independence, control, repair). Somatic noticing: where you feel money in your body when it comes up. Money conflict lives in the nervous system before it makes it into language.

Then we work with the pattern in real time. Not theoretical. The thing that happens between you when money enters the room. We slow it down, name each partner's internal logic, and build the capacity to stay in the conversation without escalation or withdrawal. Decisions come later. They're easier when the reactivity isn't running the show.

What I won't do, and what I will

I don't tell couples what to do with their money. That's not my role. My role is to help couples see clearly enough that they can decide without distortion.

I treat money as a relational system, not a technical problem. This is the emotional and relational work around money, what is known as financial therapy. I integrate it into couples therapy, intensives, and my work with executives and entrepreneurs. Most couples already have access to good advice. What they don't have is a way to stay grounded with each other and make decisions they can actually live with.

“The goal isn’t to eliminate conflict around money. It’s to make it workable.”

Read more about my couples therapy practice. The same dynamic that drives money conflict often drives the mental load asymmetry that builds in dual-career partnerships . Different form, similar clinical work.

How do you start the money conversation with your partner?

If you want to talk to your partner about money tonight without it becoming the same fight, a few things tend to help.

1. Different time, different frame. Not in the middle of a rupture, not after a credit card statement, not at 11pm. Schedule it. Frame it as: I want to understand what money means to you, not solve a problem.

2. Start with history, not the present. "What did money feel like in your house growing up?" is a different conversation than "Why did you spend that?" The first lets your partner be a person. The second puts them on trial.

3. Use the four-part question. For each of you: What is money for, for you? Security? Freedom? Status? Time? Repair of something inherited? Take turns. Don't react. Don't fix. Listen.

4. Name the emotion under the number. When the conversation gets charged, ask: What are you afraid will happen? What does this remind you of? The answer is almost never about the dollar amount.

5. Decide whether you need a third party. If the conversation cycles, escalates, or stops, that's information, not failure. It means the pattern is bigger than the two of you. That's when bringing in a [couples therapist](/couples-therapy) or a coordinated therapist-and-planner team makes sense.

If you're searching tonight because something doesn't feel right, that's information worth listening to. The fact that the conflict keeps coming back means the pattern hasn't been seen yet. Once it is, things change.

If you're in the Bay Area, I work with couples on this in three formats: couples therapy, intensives, and coordinated work with your existing financial team. The latter is built into my practice with executives and entrepreneurs. I'm at Mycelia Therapy in San Francisco, offered online throughout California.

Frequently Asked Questions

-

Money conflict is one of the most consistently cited predictors of divorce in couples research, including Gottman's. But the conflict isn't the cause. How couples engage with it is. Couples who criticize, defend, or stonewall around money tend to do the same around other topics. Money is often where the pattern shows up first and most intensely, not where it originates.

-

Financial infidelity is the deliberate concealment of financial information from a partner: hidden accounts, undisclosed debt, secret spending, lying about income or losses. Clinically, it activates the attachment system in the same way as other forms of betrayal and creates a similar before-and-after rupture. It is not less serious because it's about money. The rupture is about the breach of shared reality.

-

Avoidance is itself a money script, usually rooted in shame or family-of-origin messages that money is dangerous or corrupting. The way in is rarely confrontation. Lower the stakes: ask about history rather than the present. If avoidance persists, it's a signal that a third party (a couples therapist or coordinated therapist-and-planner team) would help.

-

Yes, and the combination is often more effective than either alone. The advisor handles strategy and execution. The therapist handles the emotional and relational material that drives reactivity around money. With written consent, I coordinate directly with clients' advisors so the two streams of work move together.

-

Neither is universally better. Intensives work well for couples who are entrenched or ready to focus and move. Weekly therapy works well when integration between sessions is part of the value. Some couples start with an intensive and move to weekly maintenance. Others do the reverse. The right format depends on urgency, capacity, and preference for pace.

About the Author

Giulia P. Davis, LMFT #157653 & Founder Mycelia Therapy

(she/any pronouns)

Giulia P. Davis, LMFT is an Italian-born, San Francisco-based Licensed Marriage and Family Therapist and founder of Mycelia Therapy and Mycelia Coaching.

Before transitioning to clinical practice, she spent 15 years as a management consultant for Fortune 500 clients, building distributed teams across three continents and eventually founding her own consultancy. She brings that same systems-thinking lens to the work she does with couples, understanding relationships not just as emotional bonds, but as dynamic structures that can be diagnosed, interrupted, and rebuilt.

Giulia specializes in working with high-achieving couples, executives, entrepreneurs, and ENM/polyamorous relationships navigating disconnection, recurring conflict, and the particular exhaustion of a life that looks successful from the outside and feels depleted from within. Her intensive and retreat offerings are designed specifically for couples who need accelerated change.

Her work combines attachment theory, Emotionally Focused Therapy (EFT), Gottman frameworks, Relational Life Therapy (RLT), and Internal Family Systems (IFS). Formats offered: weekly therapy, intensives, and psychedelic-assisted therapy.